Independent Contractor Income Thrives on Multiple Sources

Independent contractor income grows with the help of a strategy that looks beyond just the core business.

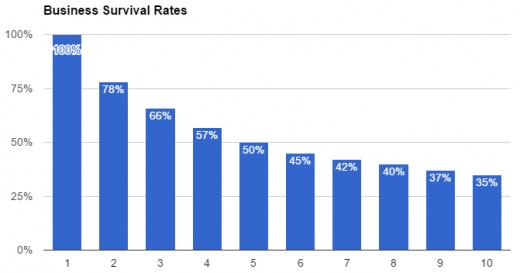

More than half of the business closures in the United States were the result of problems getting financing or a failure to reach profitability, according to the Global Entrepreneurship Monitor sponsored by Babson College.

Reaching profitability and surviving downturns often depend on a financial foundation of assets such as cash. But they also can depend on income from other sources.

Before launching a solo business, the independent contractor should develop a personal financial plan that maximizes other income and minimizes expenses. He or she also should have a reserve cash fund that can last at least six months or more.

“Starting a business can be a tremendous strain on your personal finances. It takes time before your new venture turns a profit and provides financial support for you and your family. Before starting a business, it is important to get your finances in order,” the Small Business Administration says.

A friend of mine learned the lesson in a painful way. He bought an existing business without that strong foundation. The business floundered. In despair, he committed suicide.

Source: Small Business Administration

5 Sources of Other Income

Entrepreneurs I have known have the ability to tap five or more sources of income other than what they make from the core business. They are:

- Income investments

- Freelance work

- Part-time jobs

- 401k plans

- Pensions and annuities

A new one-person business can tap these sources until the business becomes profitable or during times when business income is down. Prioritization is key.

Prioritizing Sources of Income

My ability to survive as an independent contractor and solo entrepreneur for more than 10 years depended in part on finding multiple sources of income — both inside and outside of the business.

Inside the business, I learned to develop income from sources other than my main activity, which is online management consulting. But my consulting work came first anyway because it produced the most income on an hourly basis. When I had certain days or weeks with spare time, I would focus on selling new services with a lower profit margin.

Prioritize sources of income by focusing on the highest-paying products and services first. Then pursue smaller opportunities while trying to add extra value to them.

Data: Small Business Administration. Graphic copyright 2017 by Scott Bateman

Source #1: Solo Investment Income

Some independent contractors start a solo business out of need because of a layoff or other compelling reasons such as a family crisis. Some of them have time to plan.

People with time to plan have time to save money. A portfolio of income-producing stock and bond mutual funds or exchange-traded funds can cover at least some living expenses and reduce the pressure on personal finances during tough times with the business.

It also reduces the need for a higher salary. In turn a lower salary leads to more profit and a higher profit margin.

The same concept of saving to invest for income also works well within the business. When the business has a good year and produces a strong profit, a solo business owner who uses an S corporation or C corporation tax structure can save some of that money in an investment fund.

A category of mutual funds called Income Builder Funds combines bonds with stocks that pay dividends. Some of these funds produce a 4 percent yield or higher along with the safety that comes with asset allocation. The dividends can go into a rainy day cash fund.

If the company has a bad year and needs more than just the cash fund, the solo business owner can sell shares in the mutual fund. It improves the chances of surviving until a better year.

If the investment fund is left alone, it can continue to grow and produce even more income for later years. That income contributes to the total revenue and profit of the business. It’s a labor-free security blanket.

Credit: Pixabay Creative Commons license

Source #2: Freelancing Business Income

The lone wolf works for an employer. The employer is that one person. True freelancing is hourly or project work outside of the core business.

An independent contractor may not always find enough work to fill a 40- or 50-hour workweek. Success depends in part on using every spare hour to build the business.

Here is an important question: Would you rather spend an extra five hours a week with nothing to do or spend that five hours making $5 or $10 an hour?

I chose the latter by pursuing other work such as website hosting and freelance writing. It’s better to make a little money in that five hours than none at all. More importantly, it can lead to a higher public profile, new and improved skills, and eventually to more clients.

The owner of a one-person business has a key benefit over larger companies: the flexibility to pursue freelance work. I found it was incredibly easy to change directions and adapt to new circumstances — sometimes in a matter of minutes — compared to my previous corporate job with bosses and staffs. Spare time is a chance to change directions and do freelance until the core business heats up again.

The owner of a one-person business has a key benefit over larger companies: the flexibility to pursue freelance work.

Data: Kaufmann Index of Startup Activity. Graphic copyright 2017 by Scott Bateman

Source #3: Temporary Job Income

Temporary or even long-term part-time jobs can produce extra income that once again relieves pressure on the financial security of a solo business owner.

Retail jobs in particular offer weekend and nighttime work opportunities that don’t have to interfere with a five-day, day-time business.

An outside job also relies on prioritizing the income. A part-time job that pays $15 an hour is more important to the survival of the business and the financial security of the owner than a service that pays only $5 to $10 during those spare five hours a week.

But this type of income has some negatives.

- It takes time and energy away from the business.

- It often does not result in new clients and contacts.

- It often does not produce skills and experiences that could be useful to the business.

For these reasons, temporary job income is less important than investing or freelancing.

Source #4: 401k Plans

The 55+ age group has one more advantage with a solo business if the owner worked at a company with a 401k plan.

Federal law states that withdrawing money from retirement plans such as an IRA or 401k before age 59 1/2 can result in a 10 percent penalty in addition to income taxes. But there are exceptions. For example, people can withdraw money from the 401k without a 10 percent penalty if they left their company during the year they turned 55 or older.

The 10 percent penalty does not apply to “distributions made to you after you separated from service with your employer if the separation occurred in or after the year you reached age 55, or distributions made from a qualified governmental defined benefit plan if you were a qualified public safety employee (state or local government) who separated from service in or after the year you reached age 50,” the IRS says.

A company that took over the business where my wife worked fired everyone and then offered their jobs back with a large cut in pay. Rather than take a steep pay cut, my wife retired at 55 with penalty-free access to her 401k funds if we needed them.

Source #5: Pension and Annuity Income

Research from the Kauffman Index of Entrepreneurship shows that startups by people ages 55 to 64 have climbed 60 percent between 1995 and 2016. The proportion of startups in that age group now nearly equals the other three age groups.

Older entrepreneurs that worked in companies with pensions have those pensions as a potential income source, especially if the pensions become available at age 55.

Once again, the income stream lessens the need for a higher business salary and releases money that can either go toward profits or into re-investment in the business.

This category is fifth on the list because businesses more and more are not offering pensions. As a result, the solo owner doesn’t control the outcome, unlike investing, freelancing or working part time in a job.

A solo business owner who pursues multiple sources of income will increase their chances of not just surviving but also thriving.

Putting It All Together

As it turns out, I luckily did not need to rely on investment income, temporary jobs or retirement plans. I did watch my expenses carefully and recently started to tap two pensions as I shrank my business to enjoy more free time and shift into semi retirement.

But I took steps to put all of the above tactics into place 10 years ago before I left my corporate job to start my own business. I also learned a lot about spending money carefully.

The effort gave me a great deal of confidence that I could survive any downturn. Independent contractors who pursue multiple sources of income will increase their chances of not just surviving but also thriving.